Financial Insecurity and Having "Enough" | #127

Can you ever "cure" financial anxiety with more money?

February 6th, 2021: Greetings from Taichung, Taiwan. It’s my 36th birthday today. It feels crazy to be writing that number but we can’t stop time. I feel lucky to have such amazing people in my life, doing work I love and have an amazing 2nd home in Taiwan. It was amazing to go outside after 14 days of in-home quarantine yesterday. I’m looking forward to celebrating Chinese new year in the coming weeks. Here’s a picture I took in Taiwan a couple years ago.

Thank you to Noel for the continued support and JB for becoming a paid subscriber.

#1 Can financial security be reached by earning more money?

The most common question I get from people is if I worry about retirement and if I worry about not having “enough” when I retire. People are often surprised at two things that emerge from a deeper exploration of this topic:

How little they’ve really analyzed their own relationship to money

How deeply I have analyzed it

What follows is everything I think about money, retirement, the future and a general fear of not having “enough.”

#1 Financial insecurity runs deep

Financial insecurity seems to be a proxy for all sorts of insecurities including a general fear of death, the general anxiety of rising costs of the modern world and feeling like you’ll run out of money, and not feeling like you are good enough.

Financial insecurity seems to appear in many different forms and has varying level of costs. For some it is a daily refresh of their Mint.com account, for others it is hiring a financial advisor and paying them 1% of your wealth annually for 30 years. My default mode has been to become desperate when looking for consulting work. This has led to under-pricing my work or taking project I wouldn’t have without the insecurity.

I’ve never seen of a case where anyone ever “cured” their underlying insecurities by earning more money. While I felt very comfortable while working full-time, as soon as I stopped earning that salary the insecurity re-emerged.

Counterintuitively, earning less money may help people grapple with this insecurity better which was the case for me. When I first moved to Taiwan my consulting work dried up and I made about $500 over a stretch of 4-5 months. In response I cut my spending dramatically and I learned two things: I didn’t need much to be happy and I could radically re-arrange my cost of living pretty quickly.

This did not cure my financial insecurity 100% it just made me more familiar with the feeling which enables me to know when it has a hold on my emotions and might be influencing my decision making

#2 People will spend years avoiding discomfort

People go to enormous lengths to avoid having to face these emotions directly and this is what makes quitting full-time employment so terrifying. It is not the prospect of going broke or earning less that scares people but having to be uncomfortable for long stretches of time.

After two years dealing with a health crisis earlier in my life I had some experience sitting with discomfort for long stretches of time and knew that it wasn’t all that bad and actually can lead to positive types of growth.

I didn’t think about this much when I decided to quit and was confused when people would tell me how brave I was or that they could never do such a thing because “how would they pay rent?” I took these concerns at face value as a financial calculation and didn’t really understand its about the deeper fear.

Most of the stated reasons are just not all that credible. Although they may not actually be the true source of the fear there is a problem of a lack of imagination.

Having a steady flow of income keeps you blind to the fact that when you remove this cash flow your mind will naturally start coming up with all sorts of ways to make money. My imagination for making money when I quit my job was to make money through freelance consulting. That’s it. Now I make 95% of my income through other means.

Going “back” to salaried employment is often much easier than people imagine and what people fear is that people will not accept them anymore. If I decided to go back to full-time employment I am much more confident I’d be able to find work and an arrangement that would work for me because of what I’ve learned over the past few years.

#3 People never define “enough”

Many people simply refuse to commit to a number or salary that is “enough” and even when they do they will often change it once they have reached that number. It is amazing how much wealth people will accumulate without ever realizing this fact. In addition, most people’s expectations of what they need are built on their current lifestyle and if you have head steadily increasing salaries and expenses you will assume it is only possible to live and be happy in such an arrangement

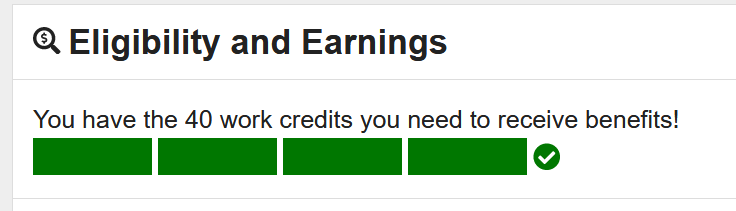

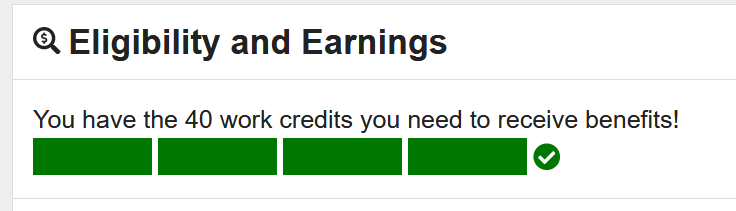

In the US you are qualified for social security when you have earned an income for 40 quarters. This includes work in high school, college and so on. I likely reached this by the age of 27 or 28.

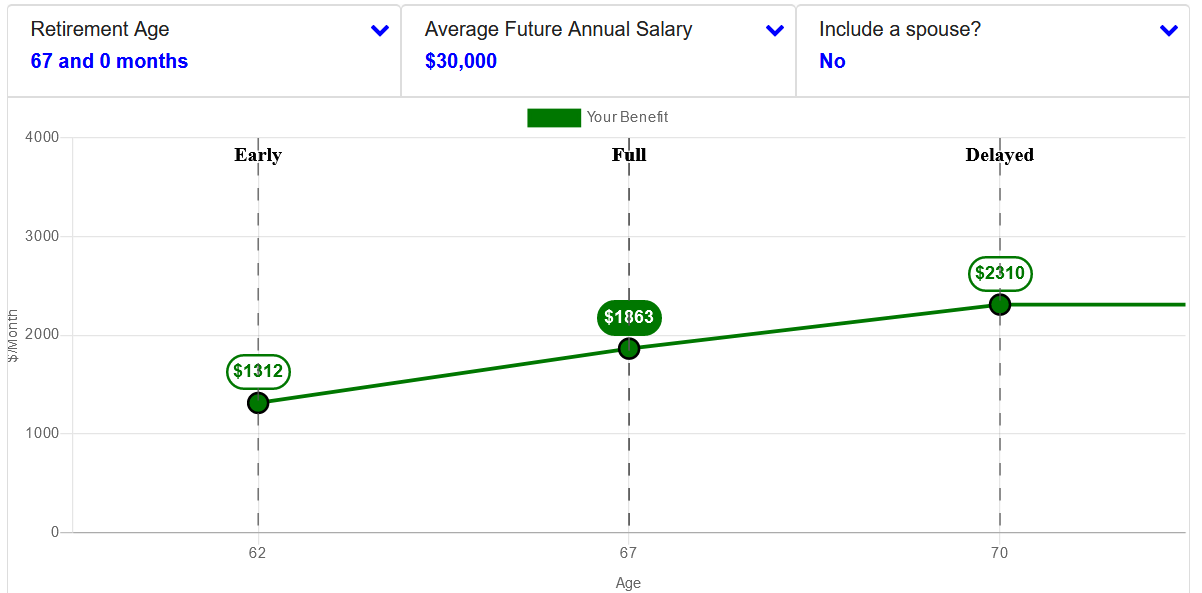

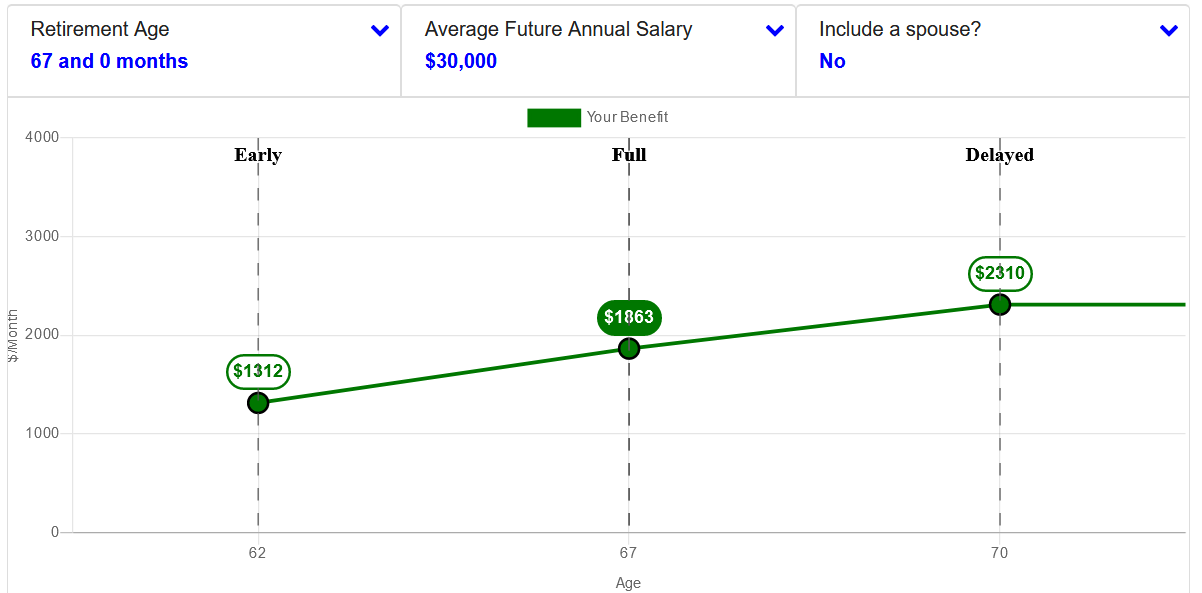

If I take some very conservative estimates like only making $30,000 a year for the next 30 years (I think I could do better but I’d be fine if this were the case) and that Angie doesn’t get a green card or ever work in the US we would still end up with $1,863 a month in retirement. Tax-free. This is pretty good!

As soon as I started working I invested like crazy. I invested about 15-25% per year of all my salaries in retirement. The stock market is 4x what it was in 2009. This seems to have paid off even though I never made a crazy amount of money. Right now if I project even a very conservative 4% annualized market return for the next 30 years, invested no additional money, and then took out the money and put it in cash and paid myself an annual salary for 25 years this would be an additional $3,423 per month (if you are ambitious you can figure out the details).

This puts me at a “retirement” of about $5,000 a month starting at age 67 based on no additional investments and that I can break even for the next 30 years. If I were to assign probabilities I would be that in 90% of my future life paths that I will do even better than this scenario.

This kind helps shift from a generalized worry about retirement to a specific stake in the ground helping to orient all my decisions. To some people $50,000 (especially in future dollars) this is way too little but for me trying to figure out how to be happy on less money is a way more interesting game to play that trying to just earn as much as possible.

I’m quite confident that even with kids we could live a really good life only making $40,000-$50,000 per year but I am also happy to admit that I am wrong when that time comes.

Other people see my life as extremely risky but I see the possibility of disaster as ruin as close to 0%. In this sense I feel my life is very risk-averse.

Defining this “worst-case” enables me to leave space for opportunities to emerge or for extended periods of non-work without anxiety.

#4 I don’t buy into the default retirement story

A lot of thinking about money and retirement comes with a default picture of work and life that says you work 40 years and then retire and live a life of leisure. I’m quite sure that this does not appeal to me. I want to be actively engaged with the world even when older.

The trick to this is discovering things you want to do even if it wasn’t something you could get paid for. Over the past few years I’ve discovered that writing, teaching, and helping people on their life and work paths is something I keep doing no matter what. All of these thigns offer the potential to make money even past the age of 67. Ideally I can do them without a need for money but it seems probable I could earn money if needed

Having faced some health issues in the past I know how fragile life is and I’m much more excited about having “pre-retirement” experiences like extended vacations with family members and friends now rather than in 30 years when my health, energy levels and ability to deal with discomfort (and cheap hotels) will be much less.

My bubble has been popped a bit on the allure of retirement. When in Mexico I was “living the dream” in a tropical location and watching beautiful sunsets every night. If this was people’s real aim in life they would move to better locations now. I think the things that matter to people - relationships, connections, creativity, love - are much harder to solve and take continuous effort and intention.

This is also why “retiring early” is overrated. The real problem never goes away. How do you spend your life?

#5 “But what about healthcare??”

Healthcare in the US is an absolute dumpster fire and probably is the most valid reason for worrying about the future.

I do worry about the future of healthcare and my ability to afford it but I also don’t see it as a good enough reason to re-orient my life around making as much money as possible through full-time employment.

After dealing with complicated dental issues, nerve damage, getting bit by a dog, an intestinal parasite, and an ear infection over the past two years the best argument for getting super rich is so that you can get access to the best doctors

Yet I also dealt with healthcare issues in other countries and realized that if health were really an issue and the US system would bankrupt me, I would move to a country where they have a better system (there are probably 20-30 countries where this is the case). I am very open to living in other countries when older which gives me a lot more financial flexibility as well.

If the US healthcare system is not fixed in the next 30 years we will have much worse problems. The resiliency I gain from hacking the healthcare system will probably be better preparation for such events than earning as much as possible!

I am intrigued to see how this resonates with people. Would you want to have a group video call on this topic?

#2 Norway’s “Rich & Equal” Trick

How does Norway ensure that service workers are not barely getting by or have to rely on welfare like in other countries like the US?

It goes back to a set of arrangements established in 1935 where labor unions from different sectors coordinated to ensure that external forces wouldn’t create a race to the bottom. What they’ve ended up with a system with higher wages for lower-skill workers which has led to a lot of automation and elimination of jobs we might see in the US. It’s really quite fascinating how it feels watching this video. Even though I’ve re-assessed my own relationship with work its hard to shake the deep rooted sense that “everyone should work, no matter what, even the low-wage store clerk making $6 an hour.”

Norway’s system has meant that a different set of work beliefs have emerged. It’s hard to appreciate how much our attitudes and beliefs of work are downstream from economic arrangements and that our work beliefs are not some divine truth. The counter to their system is that high-skill workers are paid less than they might make in other countries. I certainly know a lot of high-wage earning friends that think inequality is a problem but judging by how often they check their Mint.com net worth (surprising number of people tell me they do this daily), I doubt they would be willing to take a salary cut.

This is really why nothing like this would ever get passed in the US. In addition to the idea that your salary is your value, we pair that with the idea that if people work hard they could just land a higher-paying job.

This is an interesting debate but I think one worth re-thinking as the goal of any society is not to enable high-skilled workers to make as much as possible but to actually build a society that people want to be part of.

So suspend your default beliefs for a moment and watch, interesting part starts at 8:30:

#3 The Tom Brady Principle

In honor of the GOAT making the super bowl again I present the “Tom Brady principle” which people seem to get a kick out of.

Imagine after Tom Brady won his first Super Bowl in 2001, New England Patriots owner Robert Kraft sat Brady down and told him, “Tom, you had a fantastic season. We want to see you keep growing with the organization. We are going to promote you to General Manager.”

In sports, we would quickly question Kraft’s sanity. Yet, in the corporate world, we call this talent management.

Most of our ideas of work success are built on progression up a career ladder and we only unlock higher salaries when we move up these ladders. This creates a bad incentive of promoting people who want money, power and status but don’t care deeply about managing others.

I don’t think we should abandon this but I’d like to see more room for paying people to stay in individual contributor roles. Sales organizations usually do a good job of this because outcomes are measurable but in data & knowledge work companies really struggle to figure out how to measure performance.